Blog

Partnership Business Registration in Sri Lanka: A Comprehensive Guide

27 Aug 2024

If one is planning to start a business in Sri Lanka, the most commonly used form of business is the partnership. Registering a partnership has many benefits, but it is also accompanied by a particular legal procedure.

In this article, we will explain the entire process of partnership business registration in Sri Lanka, the documents required, and the key points.

What is a partnership?

A partnership is a type of business where two or more people engage in a business venture in as much as sharing the management, profits, and losses. The Sri Lanka Partnership Act governs partnerships in Sri Lanka and outlines the legal framework for the formation and operation of partnerships. This business structure is ideal for those people who wish to collaborate and share the workload, skills, and expertise in the business.

However, it is crucial to consider whether a partnership is suitable for your business before going through the registration process. This decision should be made depending on the type of business, the further plans and aims, and the character of the relations with the potential partners.

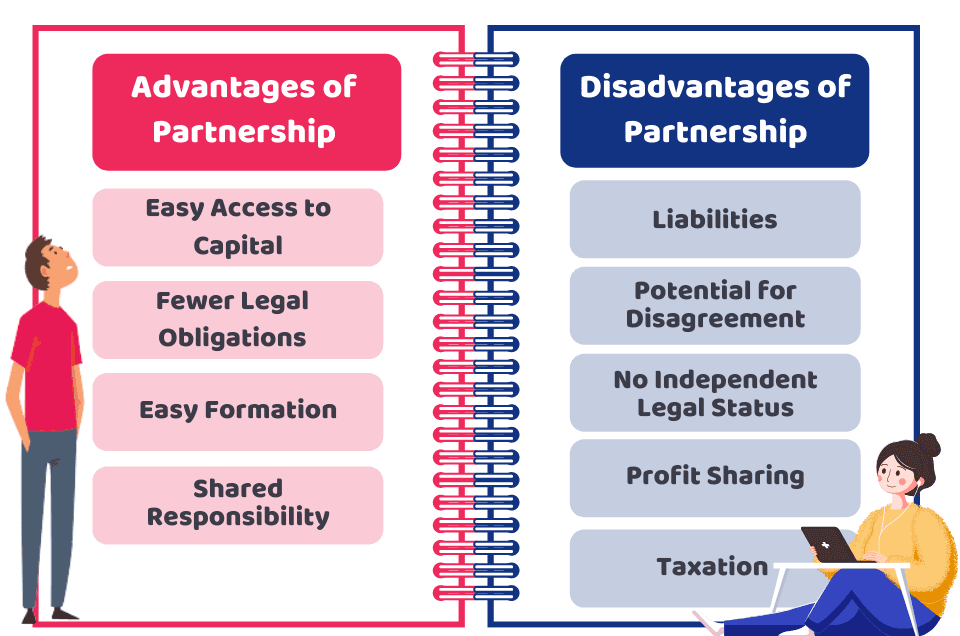

Pros and Cons of Registering a Partnership Business

Image, via accountingfirms.co.uk

Pros:

Shared Responsibility: In a partnership, the work and the duties are shared between the partners who are involved in the business, which means that each partner can concentrate on the area of specialisation, and this leads to the effectiveness of the business.

Combined Resources and Expertise: It is a fact that partners bring in different skills, knowledge, and capital (funds) that can improve the overall capability of the business and at the same time, improve the probability of success.

Simplified Taxation: Pass-through taxation is typical for a partnership when the business structure itself is not taxed. However, Profit or losses are charged to partners who include them in their individual income tax returns and this may be advantageous.

Easier Decision-Making: Partnerships are often created by a limited number of persons, which means that it is easier to make decisions and, if necessary, make changes to the existing ones.

Flexibility in Management: It is for the partners to decide how they want to run the business and there are no rigid corporate structures which give them more freedom in their day-to-day business.

Cons:

Unlimited Liability: In a general partnership, all the partners are personally liable for all the debts and other liabilities of the business. This means that the owner’s assets can be called upon to meet the loss or pay for a legal suit in case the business records a loss.

Potential for Conflicts: There may be disagreements between the partners and this may have an impact on the business if the responsibilities, rights and the division of the profits are not stated in the partnership agreement. These disputes are not beneficial for the business and strain relationships.

Shared Profits: This also means that individual partners receive less than what he or she would have received if running a sole proprietorship business based on the ratio of profit sharing.

Limited Growth Potential: Fundraising can be a little more difficult for partnerships as compared to companies because partnerships cannot offer shares. This may limit the business expansion in some way.

Lack of continuity: Another risk that may affect a partnership is when one of the partners wants to withdraw, resign or pass on. This can cause a lot of problems for the business and in extreme cases may lead to the dissolution of the business if no arrangements have been made in the event of such circumstances.

When comparing the advantages and disadvantages of a partnership, one must consider how well it will fit into the business you have planned. If you are worried about unlimited liability or want a more formal way of running your business, then a Private Limited Company might suit you. Private limited companies provide limited liability, better credibility and easier access to funds.

How to Register a Partnership Business in Sri Lanka

Registering a partnership business in Sri Lanka has several steps and requires careful attention to detail.

Here’s a detailed guide to help you navigate the registration process:

Step 1: Collect and Fill Out the Application Form

The first step in the registration of a partnership is to get an application form from the respective divisional secretary. This form will ask you to give basic details of your business, such as the names of the partners, the type of business, and the business location.

Step 2: Submit Required Documents

After the application form has been filled out, there are several documents that you are required to produce and submit.

These may include:

Photocopy of NIC (National Identity Card): Every partner is required to produce a copy of their NIC.

Land Ownership Documents: Depending on the location of the business, one will be required to present a copy of the land deed if the business is on owned land, a rent agreement if the business is on rented land, a consent letter from the land owner, and a copy of the NIC of the land owner if the business is on family-owned land.

Trade Permit: If necessary, the trade permit issued by the municipal or divisional council has to be attached.

Partnership Agreement: A signed agreement outlining the roles, responsibilities, and profit-sharing arrangements among the partners.

Additional Documents Based on Industry:

Selling goods or Importing/Exporting: A list of items you plan to trade.

Spas or Guest Houses: A police report.

Medicine and Perfumes: Approval from the Medical Supplies Division.

Ayurvedic Medical Treatment: A letter from an Ayurvedic doctor along with their ID.

Vocational Affairs: Professional qualification certificates.

Beauty Salons and Spas: Training certificates.

Nurseries or Care Centres: Approval from the Early Childhood Development Assistant.

Restaurants or cafes: Approval from the Public Health Inspector.

Step 3: Obtain Grama Niladhari Report

The Grama Niladhari report is an essential document that proves the ownership of the land and the business place.

To obtain this report, you will need to provide:

Deed of Owned Land: If the business is operated on owned land.

Consent Letter: If the land is owned by another party.

Rent Agreement: If the business is located in a rented building.

The Grama Niladhari will check the details and provide a report, which must be attached to your registration application.

Step 4: Submit Documents to Divisional Secretary

The final step is to gather all the documents and submit them to the divisional secretary’s office. If everything is in order, the divisional secretary will review your application and complete your partnership registration in Sri Lanka.

How to Draft a Partnership Agreement

A partnership agreement is a legal document that contains the terms and conditions agreed by the partners at the time of formation of the partnership. This can be express or implied, in writing or oral, but it is enforceable in law in any case. However, it is advisable to have a written contract to prevent any future misunderstandings between the parties involved.

Why is a partnership agreement important?

Conflict Resolution: Disputes or issues that may occur between the partners are solved easily because the agreement is well drafted to provide for the terms.

Streamlined Operations: It offers a clear structure of the management of the partnership business on a day-to-day basis.

Rights and Duties: It also defines the relationship between the partners in terms of their rights, obligations, and responsibilities.

Profit and Loss Sharing: It defines how profits and losses are to be shared, thus making the partners aware of each other’s operations.

Defined Roles: It clarifies the roles and duties of individual partners, which is very essential for the proper functioning of the business.

Since partnership agreements are crucial, it is wise to consult the right lawyer and engage a lawyer with a background in partnership agreements. This will help to avoid the situation when some important issues are left without regulation and protect the interests of all partners.

What Should a Partnership Agreement Contain?

Basic Information: About the business and its partners.

Capital Investment: Details on how much capital each partner will contribute.

Profit and Loss Sharing: How profits and losses will be distributed among the partners.

Business Objectives: The nature and purpose of the partnership.

Partner’s Drawings: Limitations on how much partners can withdraw from the business.

Interest on Capital: Information about interest on the capital invested and on drawings.

Partner Compensation: Details about salaries, commissions, or any other payments to partners, as well as their duties and rights.

Additional Capital and Dissolution: Conditions related to additional capital investments and the process for dissolving the partnership.

Changes in Partnership: Actions to be taken in the event of admitting a new partner, the retirement of an existing partner, or the death of a partner.

Dispute Resolution: Procedures for resolving disputes among partners.

Some of the things that should be taken into consideration and some of the tips that should be followed to ensure that the partnership registration process is successful include the following:

Clear Partnership Agreement: Should have a good partnership agreement that outlines the functions, duties, and profit-sharing arrangements of the partners. This document can help avoid future problems and guarantee the proper functioning of business processes.

Legal Compliance: Make sure that your business is in line with the laws and regulations of the country and those of the specific industry.

Conclusion

The registration of a partnership business in Sri Lanka is a wise decision for many entrepreneurs. If you follow the steps given in this guide, you will be able to register your company without any problems. Please do not forget that the main principles of successful cooperation are communication, documentation, and legal compliance.

This article gives you all the information you require to register your partnership business in Sri Lanka. If managed well and with the right assistance, one can create a good and sustainable business that will last for many years.