Blog

Mastering Payroll: What is Payroll and How to Manage It

9 Aug 2024

Payroll management is a vital activity in any organisation since it involves the processing of employees’ pay as per the legal provisions. This detailed article will discuss the payroll process, elements of a payroll report, allowable deductions, payroll records, and the pay period.

Therefore, by adopting these practices, organisations will be in a position to manage their payroll processes effectively and enhance the employees’ well-being.

Understanding Salary Components for Accurate Payroll Reporting

When preparing a payroll report, it is important to differentiate between the different parts of the salary since they are different.

Here's a detailed breakdown:

Basic Salary

The basic salary is the initial structure of the employee’s remuneration package. It is the predetermined cash wage by the employer and the employee for the job done without including other emoluments such as bonuses, allowances or other incentives. The basic wage is usually determined under the Wages Board Ordinance and does not contain any other remuneration.

Related: Difference Between Salary and Wages: A Comprehensive Guide

Liable Salary for Provident Fund and Trust Fund

The liable salary for Provident Fund (PF) and Trust Fund contributions encompasses a broader range of earnings, including:

Wages, salaries, or fees

Living allowance

Subsistence and other special allowances of the same nature

Payments for leave

Cost of food offered by the employer to the employees

Altogether, these components define the amount on which PF and Trust Fund contributions are based and meet the statutory provisions.

Taxable Salary (Liable Salary for Tax Purposes)

The taxable salary refers to all the remunerations received by the employee that are liable to tax. It is the total salary before any tax deductions and includes all allowances taken into consideration for EPF calculation. It is important to know the taxable salary so that the right tax can be reported and paid.

Net Salary

Net salary is the take-home pay which is arrived at after all the allowable deductions like income tax, PF, and any other statutory deductions have been made from the gross salary. It is the last net pay and is useful for payroll and accounting as well as for the individual’s budgeting.

The Payroll Process and Components of a Payroll Report

The payroll process involves several stages to ensure accurate and timely employee compensation:

a) Before Payroll Processing

Include Details of Newly Recruited Employees:

It is important to make sure that the payroll system is updated with all the information of the newly recruited employees. This entails their identification data, positions held, remunerations, and any other data that may be deemed pertinent. Data entry at this stage should be accurate to avoid making mistakes when processing payroll.

Exclude Details of Employees Who Have Left the Service:

Former employees should be excluded from the organisation’s payroll as soon as possible to prevent fraudulent payments. This step entails changing the status of the employee and making sure that all the outstanding payments like severance pay or any outstanding leave are computed and paid.

Keep Documents Related to Commission Payments and Miscellaneous Payments:

Keep records of any commissions, bonuses, or any other miscellaneous payments made to the employees. This documentation assists in ensuring that these payments are captured in the payroll and can be relied on during audits to be correct.

Maintain Relevant Approved Documents for Leave and Overtime:

Make sure that all the leave and overtime are recorded and authorised in compliance with the company’s regulations. This includes records of leave applications, overtime and other working allowances, and approvals that are useful in payroll processing.

Keep Documents Related to All Deductions:

Record all deductions properly with records of loans, fines and statutory deductions. This documentation helps in the right application of deductions and it is easy to defend before auditors or employees when need be.

b) During Payroll Processing

Check Deductions and Additions for Data Correctness:

Make sure that all the additional amounts which have been incorporated into the employees’ wages (for example, bonuses, the wages for overtime) and all the deductions which have been made from the wages (for instance, taxes, loans and others) are reflected in the payroll system. This step is very important to ensure that employees are paid the right wages or salaries as required.

Verify the Accuracy of All Data When Necessary:

Pay special attention to all the data related to payroll processing. This includes making sure that the details of the employees are correct, the hours worked and all additions and subtractions made are accurate. Any disparity should be resolved before closing the payroll.

c) After Payroll Processing

Validate and Certify the Correctness of the Payroll:

Last but not least, make sure that the prepared payroll is checked and signed. This involves verifying the payroll report to ensure that all the records are genuine and the employees are paid the right amount.

Ensure the Payroll is Approved by the Concerned Officer(s):

Obtain permission from the appropriate authorities for instance the heads of finance or human resources. This step assists in ensuring that the payroll is authorised and is fit for processing so that payment can be made.

Forward the Approved Payroll to the Relevant Departments for Payment:

Forward the approved payroll to the finance or accounting department for salary payments.

Procedure for Preparing a Payroll

Image via, quickbooks.intuit.com

A formal procedure for preparing a payroll ensures accuracy and compliance with labour laws.

The payroll report is typically divided into several parts:

Part I: Employee Identification:

Employee Number of the Institute: An identification number that relates to the specific individual of an employee.

Employee's Provident Scheme Registration Number: These are required while making payments towards the provident fund.

Name: Name of the employee with his or her first and last name.

Gender: Gender of the employee.

Age: Age of the employee.

Position: The designation of the employee at the company.

Grade: This one is a little more specific and can be defined as the position’s rank or hierarchy level within the company.

Hours Worked: The sum of all hours that an employee has worked during the pay period leading up to the pay cheque.

Part II: Consolidated Salary:

Basic Salary: The fixed base pay for the employee.

Budgetary Allowances: Additional allowances as per the company’s budget policies

Part III: Additional Payments and Deductions:

Deductions due to commencement of service in the middle of the month: Pro-rata salary adjustments.

Leave without pay and related deductions: Deductions for unpaid leave.

Late arrival and related deductions: Penalties for late arrivals.

Payments for working on holidays: Additional pay for holiday work.

Addition of salary arrears: Back pay adjustments.

Addition of commissions: Commission earnings.

Food allowances: Allowances for meals.

Living allowances or similar allowances: Housing or cost of living allowances.

The sum of Part II and Part III forms the basis for contributions to the Employees' Provident Fund (EPF) and Employees' Trust Fund (ETF).

Part IV: Other Earnings:

Overtime allowances: Overtime wages for the extra hours of work done.

Attendance incentives: Extra incentives for punctuality and presence in class.

Product incentives: Performance-based bonuses.

Accident allowances: Reimbursement for injuries sustained at the place of work.

Night shift allowances: More wages for the night shift workers.

Telephone bill reimbursement: Allowance for business-related calls made by the employees.

Transportation expense reimbursement: Meals and Accommodation expenses.

Fuel expense reimbursement: Reimbursement for fuel expenses incurred in the course of performing their duties.

House rent reimbursement: Housing allowance.

When Part IV is added to the EPF and ETF contribution basis, it forms the gross salary, which is the tax basis.

Part V: Deductions:

8% for EPF: Employee’s contribution to the provident fund.

Stamp duty: Legal tax on salary.

Tax payable on earnings (APIT): Advance Personal Income Tax.

Salary advances: Deductions for salary advances taken.

Insurance schemes: Premiums for employee insurance.

Savings schemes: Deductions for employee savings plans.

Basic value of foods: Costs of meals provided by the employer.

Accommodation or house rent charges: Rent for employer-provided housing.

Employees' security deposit: Security deposits are required by the employer.

Value of goods purchased: Deductions for goods bought on credit.

Employee fines (disciplinary grounds): Penalties for misconduct.

Loan instalments taken from the company: Repayment of company loans.

Payments to a third party at the employee's request: Authorized third-party payments.

Contribution payments to a sports club: Membership fees for sports clubs.

The net (residual) salary is obtained after all authorised deductions are made from the gross salary.

Part VI: Company Contributions:

3% company contribution to ETF: Employer’s contribution to the trust fund.

12% company contribution to EPF: Employer’s contribution to the provident fund.

Total contribution to EPF: Total of the contributions of the employer and the employee.

Date of wage payment: The day on which salaries are paid.

Employee's signature: The following is the acknowledgement of receipt by the employee.

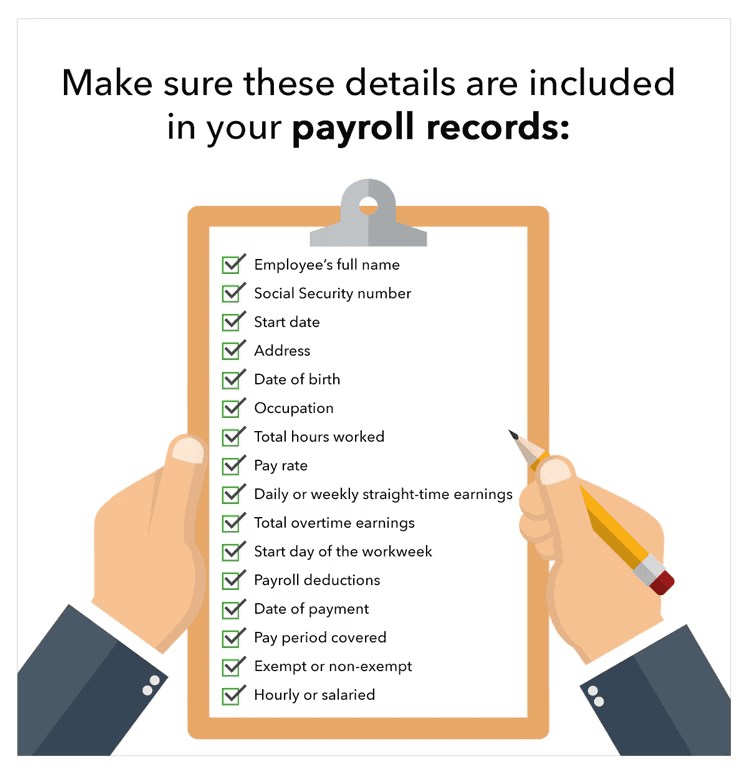

Records You Must Maintain Regarding Payroll

It is crucial to keep accurate records of the payroll and its information to ensure compliance with the law and organisational policies and to avoid confusion and delays.

Key records include:

Service Records:

Service records should be kept for at least six years and include:

Employee's Full Details: Full name, address, date of birth, gender, marital status.

Employment Details: Dates of appointment, positions held, grades, probationary periods, starting salary, salary scale and other allowances.

These records should be updated from time to time, to accommodate any change in the employee’s status or remuneration.

Attendance Records:

It is important to keep different records regarding attendance for each of the workers.

These reports should include:

Basic Details: Name of the Employee, His position, Date he joined the company.

Attendance Information: Date of joining, date of reporting to work, date of relieving from work, leave balance, leave taken.

The records of attendance are useful in determining the salaries to be paid, evaluating the performance of the employees and checking whether the company is meeting the legal requirements of the country.

Payroll Transaction Records:

In the case of every employee, there should be records of the salaries and wages paid to him or her.

These should include:

Industrial Period: Specific period for which wages are paid.

Work Details: Working hours, working days.

Salary Components: Normal pay, extra pay, productivity bonus.

Acknowledgement: Endorsement of the receipt of salary by the employee.

These records are useful for auditing and payroll and in case of any dispute, they are useful in settling the same.

Salary Disbursement Period

To make sure salaries are paid on time, some rules set specific deadlines for when payments should be made.

These rules are found in the Shop and Office Workers Act and the Wages Board Ordinance.

Shop and Office Workers Act:

According to sub-section (b) of section 19 (1):

If such a period does not exceed one week, the payment has to be made within three days from the end of such period.

In the case of a period that extends beyond one week but does not exceed two weeks, payment has to be made not later than five days after the end of the period.

If the period amounts to more than two weeks, then it must be paid within ten days from the end of the said period.

Special Note: If an employee's service is terminated by the employer or the employee permanently leaves, the employer must pay the due remuneration before the end of the second working day after the termination date.

Wages Board Ordinance:

According to sub-section (b) of section 2 in Part I:

If the period does not exceed one week, payment must be made within three days after the end of the period.

If the period is more than one week but not more than two weeks, payment has to be made within five days from the end of the period.

If the period is above two weeks, payment should be made within ten days from the end of the period.

Special Note: If for any reason the wages cannot be paid within the prescribed period the employer may hold the wages and pay the worker as soon as possible after the expiry of the prescribed period where the worker is absent or for any other justifiable cause.

Additional Special Note: Employment can be terminated by the employer or the worker may decide to quit permanently, in such cases the employer is supposed to pay all due wages before the end of the second working day after the termination of the worker’s employment.

Conclusion

Payroll management is a crucial component of any organisation. Therefore, when the business understands the makeup of salary and wages, the payroll process, and record-keeping, this will help to meet the legal standards and also increase satisfaction among the employees.

Payroll should be efficient, that entails paying the correct amount at the right time, following the laid down rules and regulations, and record keeping. In case you need help with the management of the payroll and compliance issues, it is recommended to turn to PDMC Free Consultation.

This article is a one-stop guide that covers all the fundamentals of payroll management to ensure that organisations’ payroll procedures are efficient and employees’ morale is high.